Month: April 2026

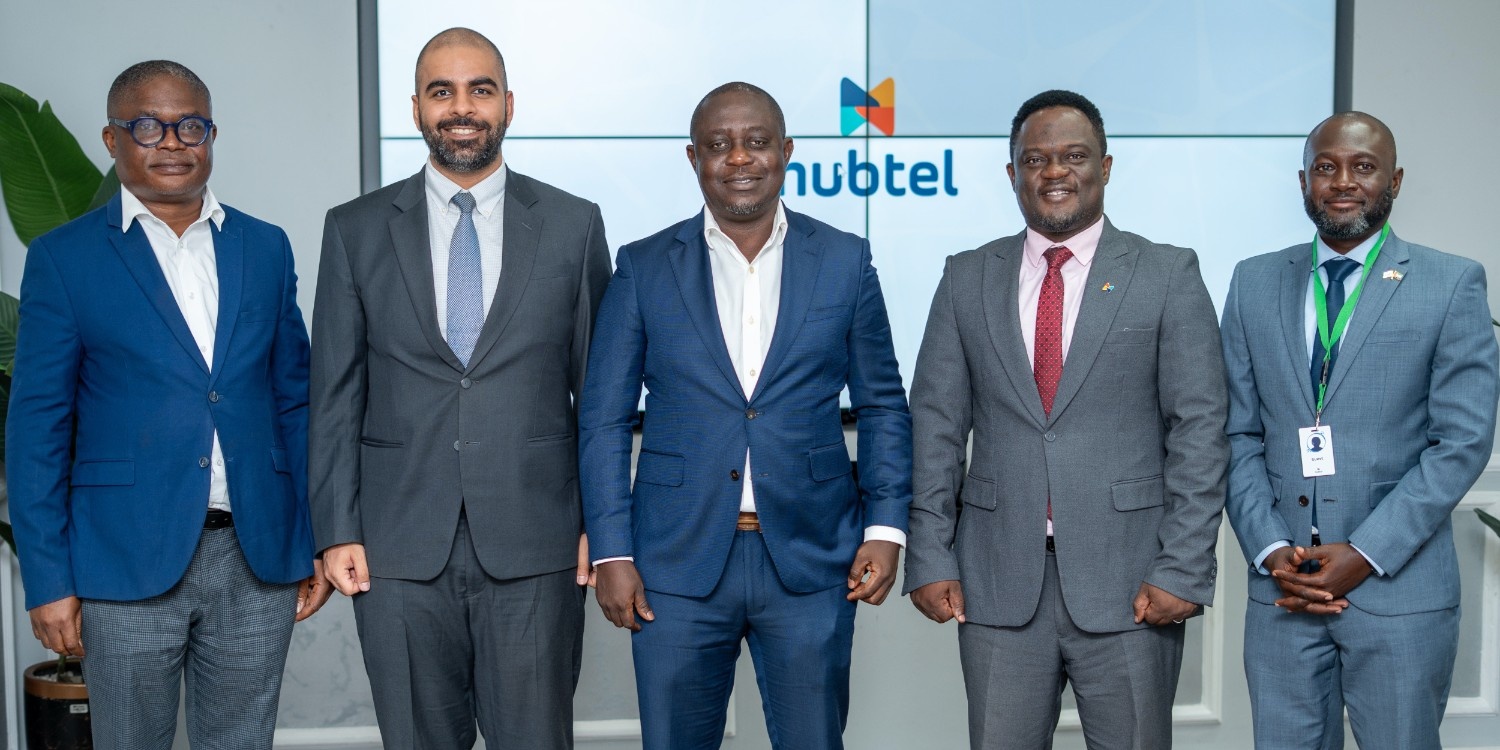

Absa Group CEO Engages Hubtel Leadership on Financial Innovation and Collaboration

Group CEO of Absa, Mr. Kenny Fihla met with General Manager, Ernest Apenteng along with the leadership teams of both companies over a lunch meeting as part of his official visit to Ghana.

The meeting focused on shared opportunities and how both companies can strengthen the long-standing collaboration between Absa and Hubtel.

Advancing the Credit Economy

Discussions covered activity in the credit space, including digital credit and Buy Now, Pay Later services. Hubtel shared insights from a live pilot granting transactional loans to users on selected apps, which is seeing strong adoption and growth. Opportunities to deepen collaboration in the credit space were also explored, building on the work of an existing joint technical committee.

Unlocking SME Financing Opportunities

Both organisations acknowledge that access to credit for small and medium‑sized enterprises (SMEs) remains a largely untapped opportunity, and strong alignment on the need to develop innovative solutions to address this gap and support inclusive economic growth.

Accelerating Partnerships and Strategic Alignment

Mr. Kenny Fihla proposed expanding the joint technical engagement to enable faster execution and broader impact. There was also discussion on establishing a regular platform to review strategy, innovation, and partnership opportunities across payments, credit, and digital finance.

Impact in Revenue Mobilisation

Hubtel’s work with the Accra Metropolitan Assembly (AMA) was also cited in the context of public sector revenue collection. Since the initiative began in late 2024, collections have grown year-on-year setting new record revenue collections for the AMA each year. Revenue collection for AMA has grown by over 550% since the new system was deployed fully from January 2025 to December 2025.

Absa offered support to collaborate with Hubtel to expand similar services to other assemblies and local authorities across the country.

READ ALSO: Hubtel Hosts Leaders of the UK Department for Business and Trade

Ghana’s fintech ecosystem continues to evolve across payments, credit, and digital finance as collaboration between bank, mobile money providers and payment service providers deepens.

Both the leadership from Absa and Hubtel resolved to press forward with plans to work even more stronger together through technical collaborations to expand their payments infrastructure, support customers in accessing digital services and ultimately grow transaction volumes.

Related

Hubtel Hosts Leaders of the UK Department for Business and Trade

April 10, 2026| 3-minute read

When Communication Became Money: Revisiting Hubtel’s Pivot into Payments

March 26, 2026| 5-minute read

Hubtel Empowers Next Generation Through AI Education Partnership with Brainwave AfricaTech

March 3, 2026| 5-minute read

Clearer Account Names on Your Money Page

Running a business is easier when you can tell exactly where your money is at a glance. We have updated the account names on your Money page to better reflect how you receive and send funds every day.

New Names, Clearer Purpose

The previous labels, POS Sales Account and Prepaid Account, no longer fully described how merchants use the platform. We have updated these names to align with the actual flow of your money:

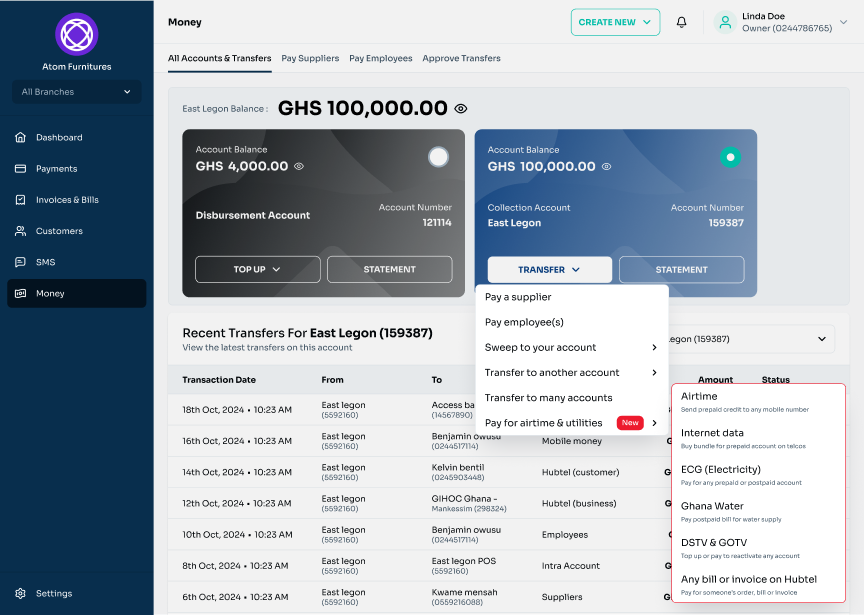

- Collections Account (formerly POS Sales Account): This is the dedicated account where you receive all payments from your customers.

- Disbursement Account (formerly Prepaid Account): This is the account you fund when you need to send money out, such as funding SMS campaigns, API and commission services.

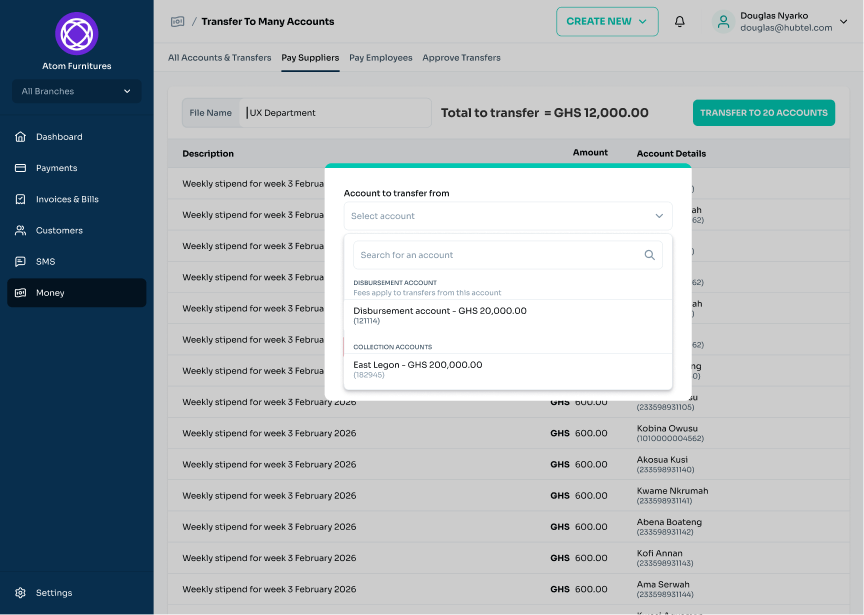

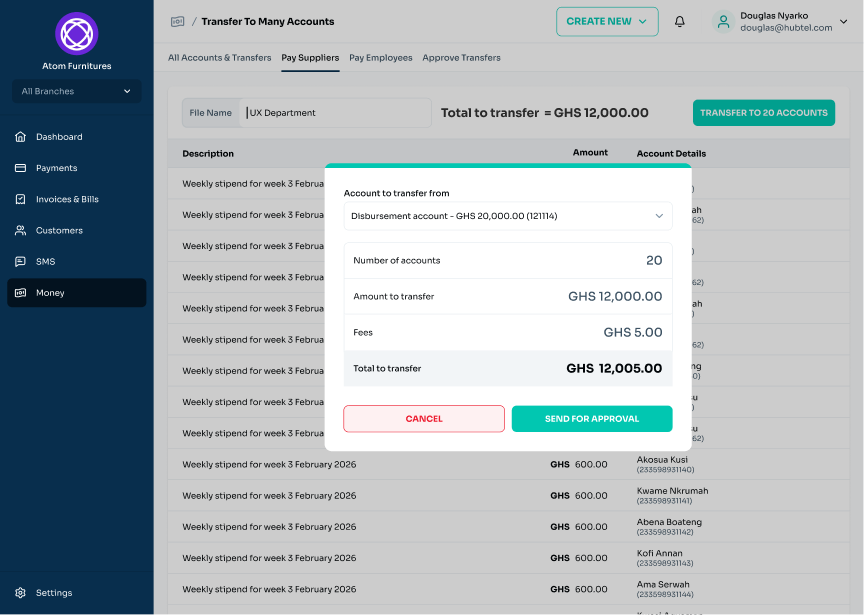

Better Visibility for Paying to Many Accounts

Alongside these clearer labels, we have improved how you handle outgoing transactions:

- Pay Many Accounts: You can now make payments to multiple accounts at once using your Disbursement Account.

- Transparent Fees: Every payment to many accounts now includes a clear breakdown of fees, giving you full visibility into your costs before you send money.

What This Means for You

This is a naming update designed to make your experience more intuitive.

- No Action Required: Your account balances and transaction history remain exactly the same.

- Unchanged Workflows: You can continue to use your accounts as you always have, just with labels that are easier to understand.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Your Laundry Customers Will Pay. They Just Need a System That Asks

May 28, 2026| 2-minute read

Upcoming Changes: Do More in One Place

April 23, 2026| 2-minute read

Introducing a New Way to Log Into Your BackOffice

April 10, 2026| 2-minute read

Upcoming Changes: Do More in One Place

For many businesses, managing money goes beyond receiving payments to include buying airtime, settling utility bills, and tracking constant fund movements. Often, this leads to a marathon of app-hopping.

One minute you are logged into a bank portal, the next you are switching to a mobile money app, and later you are using a separate website just to settle a bill. This jumping between tools wastes time and makes it difficult to see the full picture of your finances.

The Backoffice Portal is addressing this with new features designed to bring these everyday financial activities into a single, unified workspace.

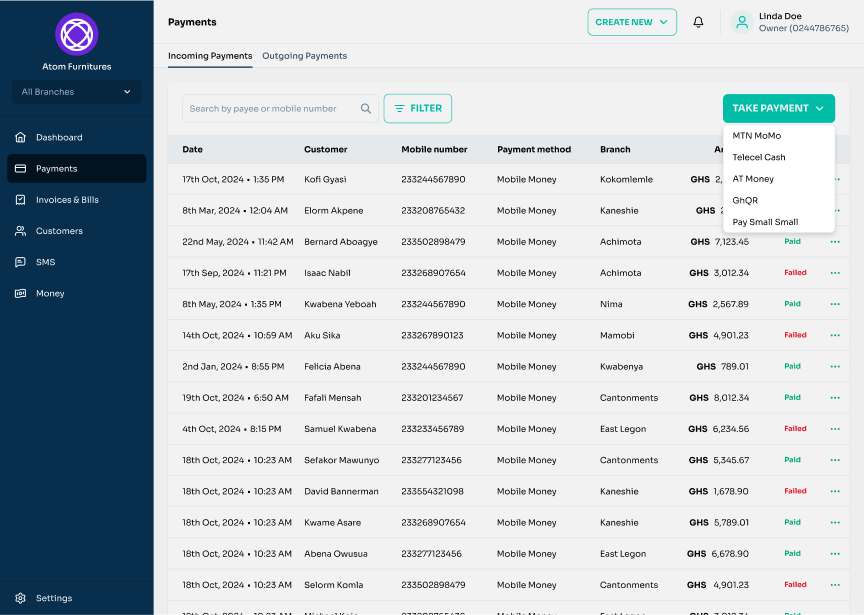

Never Miss a Sale: Start collecting payments right here.

With the new Take Payments feature, the process of requesting payments is built into your BackOffice. You can initiate customer payments through mobile money, GhQR and other supported channels. This makes it easier to collect funds quickly while ensuring every incoming transaction is tracked in one system for simpler reconciliation.

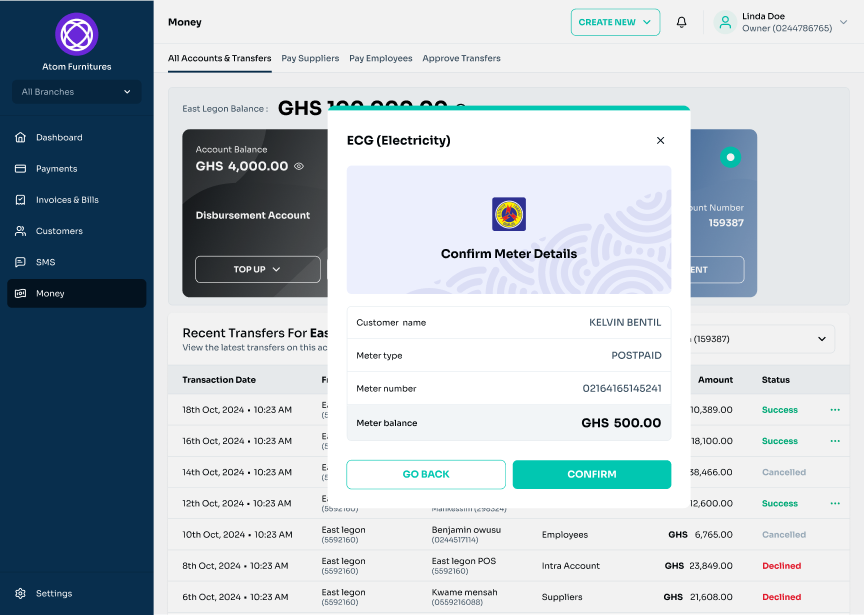

Pay Your Bills Directly from Your Back Office

At the same time, managing business expenses is now just as convenient. You can pay for essential services like electricity (ECG), water, and TV subscriptions (DStv, GoTV) directly from your Backoffice. You can even handle airtime and data purchases for your team in the same place. Moving these tasks into your main workflow saves time and reduces the risk of missed payments.

Better Visibility for Better Decisions

These updates are built around how your business operates. Taking payments and paying bills are ongoing tasks and bringing them together means fewer interruptions and a more organized way to manage your cash flow. By keeping more transactions within the platform, you gain better visibility to track your balances, monitor activity, and make informed decisions.

Get Ready to Explore the New Features

The new take payment and billing services will soon be ready for you on Backoffice Portal. This update lets you collect customer payments and pay your bills directly from your Portal. Because everything is built into one hub, you can manage your money and run your business daily without having to jump between different apps or websites.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Your Laundry Customers Will Pay. They Just Need a System That Asks

May 28, 2026| 2-minute read

Clearer Account Names on Your Money Page

April 23, 2026| 2-minute read

Introducing a New Way to Log Into Your BackOffice

April 10, 2026| 2-minute read

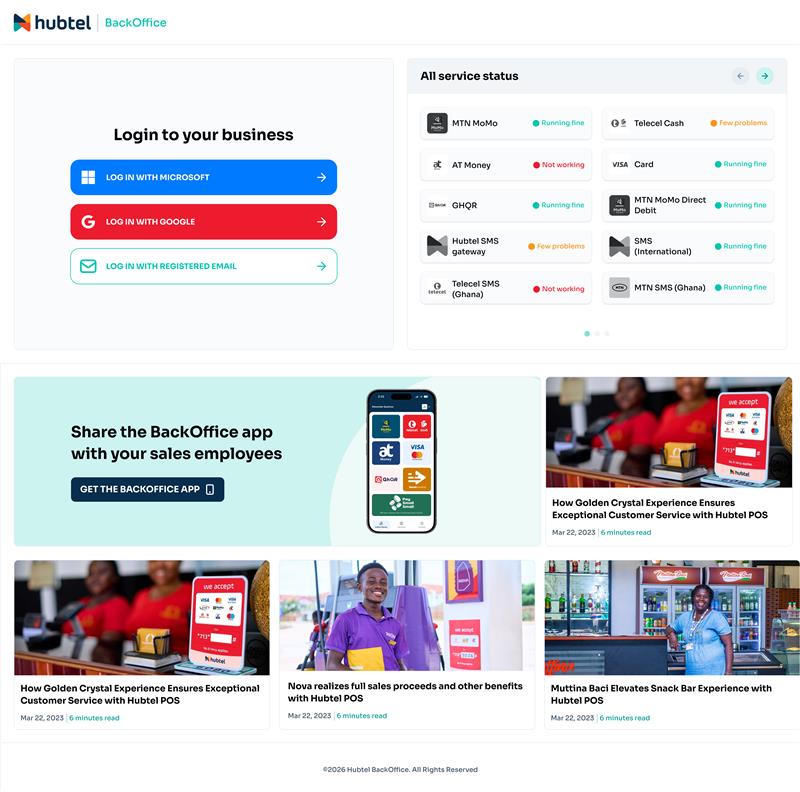

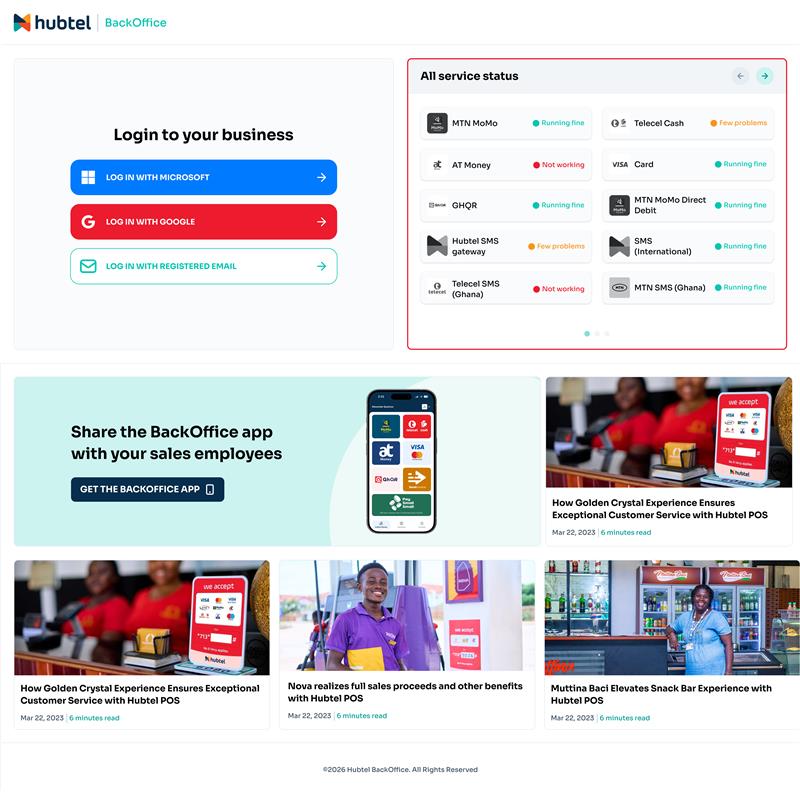

Introducing a New Way to Log Into Your BackOffice

When you’re ready to start your business day, the last thing you need is a login process that leaves you in the dark. You need to know if your payment channels are running smoothly before you even begin processing transactions. We’ve redesigned the Backoffice login page to give you a clear view of your business tools and system performance from the moment you arrive.

A More Secure Way to Sign In

Managing a business means protecting your financial data. We have refined the login process to add extra security without slowing you down.

- Microsoft and Google Logins: You can still use your existing accounts, where you receive a One-Time Password (OTP), which is sent to your registered phone number for extra protection.

- Registered Email Login: OTP codes are now sent to your email. This ensures you can access your account even if you are outside Ghana.

Check Service Status at a Glance

Now, you can see the real-time performance of all key services directly on the login page.

With the Service Status dashboard, you can:

- Confirm if payment and notification channels are “Running fine”.

- Identify ongoing issues to avoid transaction delays.

- Make informed decisions when handling customer transfers or payments.

Stay informed on Backoffice changes

You shouldn’t have to hunt for information about new features or system changes. The login page now includes a dedicated News section that brings important updates directly to you.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Your Laundry Customers Will Pay. They Just Need a System That Asks

May 28, 2026| 2-minute read

Clearer Account Names on Your Money Page

April 23, 2026| 2-minute read

Upcoming Changes: Do More in One Place

April 23, 2026| 2-minute read

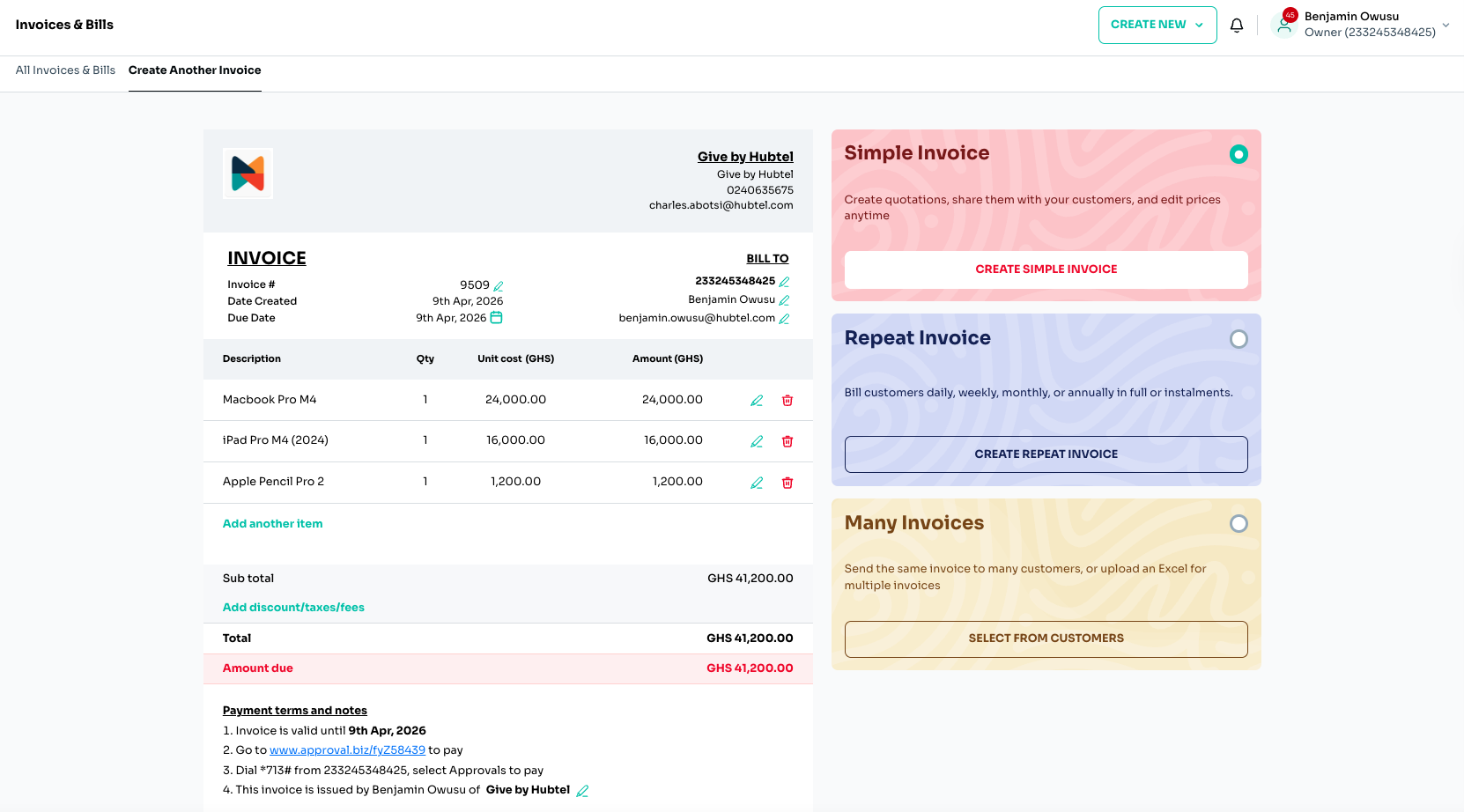

Billing is Now Smarter, Faster, and More Flexible

Let’s be honest: creating and managing invoices shouldn’t feel like extra work. Whether you are billing a single customer, setting up recurring payments, or invoicing an entire group, you need the process to be quick and straightforward. We have upgraded the Invoices & Bills experience to do exactly that.

A Better Way to Create Invoices

The invoice creation process is now smoother from start to finish, with all necessary fields organized in one view.

- Quickly add customer details under Bill To, enter invoice numbers, and set due dates.

- Add items with quantities and prices, and watch your totals update instantly as you work.

- Easily apply discounts, taxes, or additional fees without extra steps.

The Right Invoice for Every Need

One size no longer has to fit it all. You can now choose a specific invoice type based on how you bill your customers:

- Simple Invoice: Best for one-time purchases or single services, like a quick repair or consultation.

- Repeat Invoice: Ideal for recurring payments (daily, weekly, monthly, or yearly). This is perfect for high-value items, such as school fees or electronics, that customers pay for in instalments.

- Many Invoices (Group Billing): Designed for bulk billing. You can send the same invoice to a group or upload a list with different amounts, useful for charging rent to tenants or fees to a group of students.

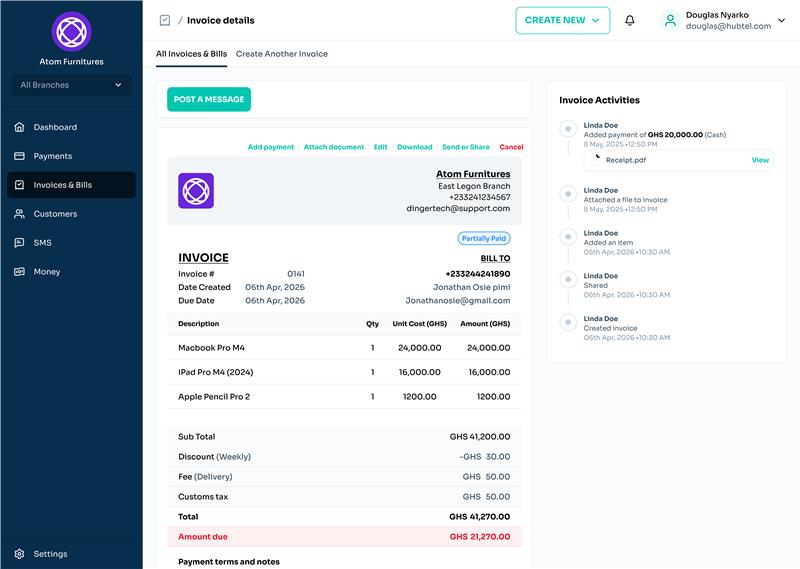

Manage Everything in One Place

Once an invoice is created, you no longer need to switch between screens to track its progress.

From a single view, you can now:

- Track Status: See instantly if an invoice is “Paid” or “Not Paid”.

- Log Manual Payments: Record payments made via cash or check so your records stay accurate.

- Monitor Activity: View a complete timeline of all activity related to that specific invoice.

- Share and Edit: Download, share, or attach necessary documents directly to the invoice.

Try it Out

The new Invoices & Bills experience is live. Log in today to see how these updates help you reduce errors and manage your billing with less stress.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Your Laundry Customers Will Pay. They Just Need a System That Asks

May 28, 2026| 2-minute read

Clearer Account Names on Your Money Page

April 23, 2026| 2-minute read

Upcoming Changes: Do More in One Place

April 23, 2026| 2-minute read

Hubtel Hosts Leaders of the UK Department for Business and Trade

Ghana has moved from the margins of the global digital economy conversation to the centre of it. And the world is starting to show up to prove it.

The UK Department for Business and Trade visited Hubtel for a high-level strategic engagement. Leading the delegation were Mark Smithson, Regional Director for Anglophone West Africa, and Jo Ann Sackey, Country Director.

The conversation centred on Ghana’s digital economy, fintech innovation, and what deeper UK-Ghana collaboration could look like from here.

The discussion covered the Department for Business and Trade’s mandate in depth, from supporting businesses looking to grow across borders, to connecting companies with in-market partners and networks, to facilitating introductions between established players and emerging ones across the continent.

The engagement also opened space for longer-horizon conversations, including Hubtel’s expansion strategy and what potential capital market opportunities could signal to global investors about the strength and maturity of African homegrown technology.

Jonathan Ansah, Chief Financial Officer of Hubtel, who was present at the meeting, noted that the discussions were as practical as they were strategic.

“We explored several areas where collaboration could be beneficial, from market entry support to the networks the Department for Business and Trade brings to the table. The conversation was forward-looking.”

He added that the visit reinforced something broader. “The way we see it, when the right opportunity presents itself, you want to already have your house in order. And these conversations are part of that process.”

Mr. Smithson, reflecting on Ghana’s position in the regional picture, said;

“Our interest in Ghana’s digital economy reflects a strong belief that the country is emerging as one of Africa’s most dynamic hubs for fintech and digital trade.”

He added that “The UK has become a natural springboard for African fintech founders, offering advanced financial systems, strong regulation, and deep capital markets.

We see real potential in partnerships that combine Ghana’s technological strength with the UK’s global reach, enabling companies to scale internationally and accelerate investment flows.”

The question is no longer whether African fintech belongs in the global conversation. It is how quickly the right partnerships can turn that conversation into action.

READ ALSO: Cornell University Visits Hubtel To Understand Ghana’s Digital Economy

This was not just a courtesy call, but also a signal that the conversations shaping the future of digital trade in West Africa are happening here, and Ghana-based companies are increasingly part of them.

About Hubtel

Hubtel is a Ghanaian technology company licensed by the Bank of Ghana as an Enhanced Payment Service Provider. The company enables businesses of all sizes to accept payments (mobile money, cards, and QR), manage transactions, and connect with customers through messaging and commerce.

Individuals can also use the Hubtel App to pay bills, order goods, send money, and more.

Hubtel currently operates 12 offices nationwide and has over 600 employees across the country. Founded in 2005, its mission is to drive Africa forward by enabling everyone to find and pay for everyday essentials, building a platform that helps every person and business take part in the digital economy.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Hubtel Hosts Leaders of Dubai Chambers Ahead of New Horizon Investment Forum

May 15, 2026| 3-minute read

Absa Group CEO Engages Hubtel Leadership on Financial Innovation and Collaboration

April 28, 2026| 2-minute read

Hubtel Joins MTN to Combat Fraud Via Fintech Partner Exchange

April 9, 2026| 5-minute read

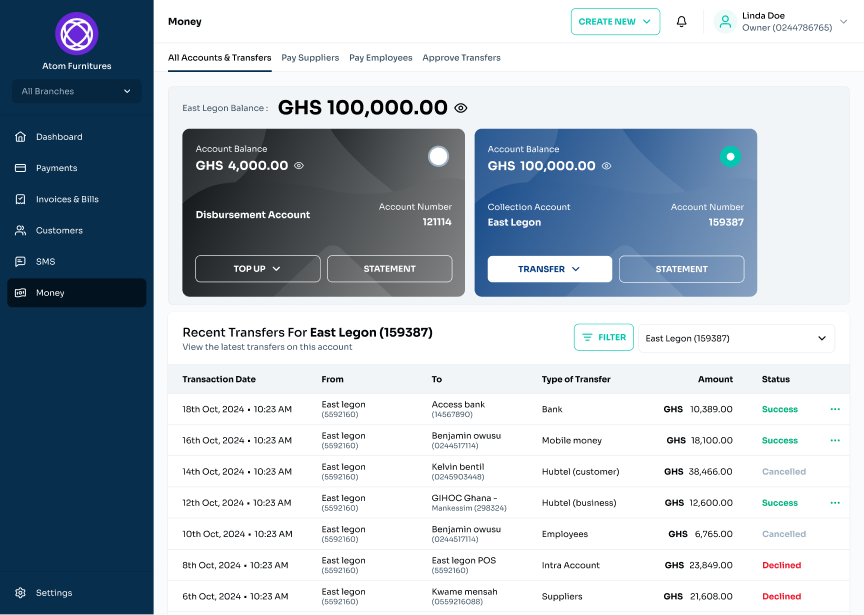

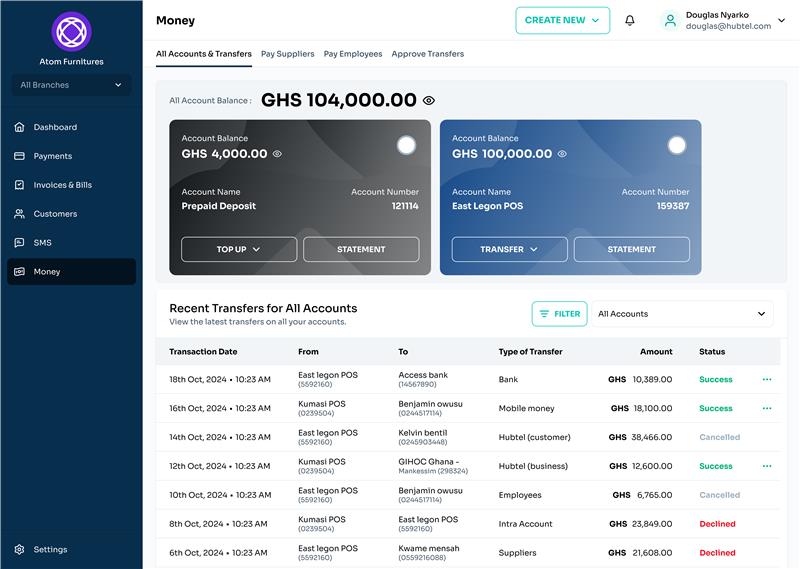

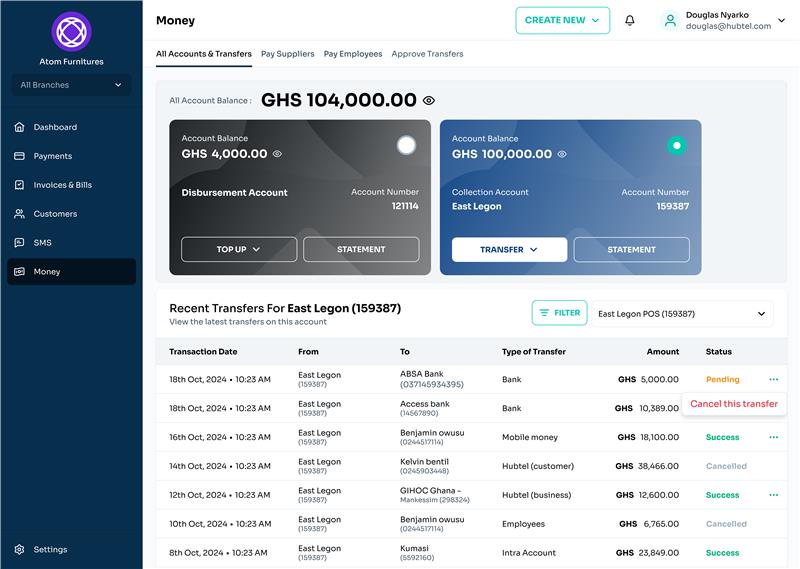

Manage Your Money with Ease

Running a business means keeping a close eye on what’s coming in, what’s going out, and what’s available at any moment. When your finances are scattered across different menus, it slows you down and creates unnecessary stress.

We have redesigned the Money page on your Backoffice to give you better visibility and faster access to your funds.

See Your Money in One Place

No more switching between screens to track different accounts. The new layout provides a complete overview of your finances at a glance:

- Total Balance: Instantly view the combined total of all your accounts.

- Individual Accounts: See clear, separate cards for each account to identify where your funds are held.

- Detailed Statements: Access a clear breakdown of every deposit and withdrawal, which you can download for your records at any time.

Simplified Navigation

We have reorganized the side navigation menu so all “money” functions are in one place. Everything you need is now just a click away, making your workflow smoother and more professional.

- Approvals and Pending Payments: You can now manage requests directly from the dropdown menu in the top-right corner.

- Owners with approval rights can view and manage pending requests.

- Finance Managers can easily track and manage pending payment requests.

- Cancel Transfer Request: If an employee makes a mistake, they can now cancel an approval request before it is processed to ensure incorrect payments aren’t accidentally approved.

Try it Out

The new Money page and dashboard updates are live today. Log in to your Backoffice to explore these features and see how they transform your daily management.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Your Laundry Customers Will Pay. They Just Need a System That Asks

May 28, 2026| 2-minute read

Clearer Account Names on Your Money Page

April 23, 2026| 2-minute read

Upcoming Changes: Do More in One Place

April 23, 2026| 2-minute read

Hubtel Joins MTN to Combat Fraud Via Fintech Partner Exchange

For many Ghanaians, mobile money has quietly replaced the traditional bank. Sending money across regions, paying for services, and running daily transactions now happens in seconds, without stepping into a banking hall.

That convenience has reshaped how people live and work. At the same time, it has introduced a reality that the ecosystem can no longer treat in isolation: fraud in digital payments.

Operating within Ghana’s fast-evolving payments landscape means engaging with fraud not as a distant risk, but as a live, cross-system challenge that follows the flow of transactions rather than staying within the boundaries of any single platform.

Fraud is no longer contained within individual systems. As interoperability deepens across platforms, fraudulent activity increasingly moves along the same pathways as legitimate transactions, exploiting gaps between institutions rather than weaknesses within one.

In such an environment, visibility becomes fragmented. No single institution has full end-to-end oversight across the entire transaction chain, yet each remains responsible for ensuring secure and reliable processing within its own domain. This creates a structural challenge that cannot be solved in isolation.

A significant portion of fraud does not originate within payment platforms themselves. In many cases, it begins outside the system through social engineering, user manipulation, or compromised credentials.

By the time a transaction is initiated, the system is often processing inputs that appear valid, even though the user behind them has already been influenced.

READ ALSO: Hubtel Awarded Overall Best Fintech Partner at the MobileMoney Fintech Stakeholder Dinner & Awards

This distinction is critical. Fraud detection is not only about identifying technical anomalies within a platform, but also about recognizing behavioral signals that suggest compromised intent.

Without coordinated intelligence across institutions, identifying these patterns early enough becomes significantly more difficult.

These perspectives were reinforced during the Fintech Partner Exchange on Fraud and Collective Action hosted by MobileMoney Limited on April 2, 2026. The dialogue brought together stakeholders across the payments ecosystem to examine how collaboration can strengthen collective defenses against fraud.

Representing Hubtel, leaders including Mr Ernest Apenteng (General Manager), Godsway Akakpo (Revenue Assurance Manager), Francis Wilson (Head, Infrastructure and Payment), and Ebenezer Boffour (Head of Internal Affairs) were present at the engagement.

Speaking during the panel session, Mr Boffour highlighted a core reality: many fraudulent transactions enter the system after users have already been compromised externally.

“Once a user has been compromised, the transaction often proceeds as instructed. The real challenge is identifying such situations early enough to intervene,” he noted.

This underscores a limitation that platforms face individually. While internal monitoring systems can detect anomalies within their own environments, intervention is often most effective before a transaction is executed, when signs of compromise can still be intercepted.

This view aligns with broader industry insights shared during the dialogue. Clara Bawah Arthur, CEO of Ghana Interbank Payment and Settlement Systems (GHIPSS), emphasized that interoperability in payments inherently extends to interoperability in fraud.

As systems become more connected, fraudulent activity can traverse platforms just as easily as legitimate transactions, making isolated defences insufficient.

Similarly, Joshua Edmondson, Board Chair of the Mobile Money Agents Association of Ghana, pointed to the role of user behaviour in fraud prevention, noting that many cases stem from users unknowingly disclosing sensitive information under pressure or deception.

From our standpoint, these insights reinforce a central principle, that fraud in a connected payments ecosystem is both a behavioural and systemic issue. Addressing it effectively requires coordinated visibility, shared intelligence, and aligned responses across institutions.

While platforms continue to strengthen internal controls, those measures alone are not sufficient in an environment where fraud can originate externally and move across multiple systems.

The ability to detect, share, and act on signals collectively is becoming just as important as the ability to process transactions securely at the platform level.

As Ghana’s digital payments ecosystem continues to expand, the pace and volume of transactions will only increase. With that growth comes both opportunity and risk.

Interoperability has made payments more accessible and efficient, but it has also created pathways that require stronger collective safeguards.

Sustaining trust in digital payments will depend not just on the strength of individual platforms, but on how effectively the ecosystem works together to protect it.

Fraud prevention in this context is not a standalone function. It is a shared responsibility that requires continuous collaboration, real-time intelligence, and coordinated action across all participants in the payments value chain.

Trust remains the foundation of digital financial systems. Protecting it will require more than isolated efforts. It will require a connected response to match a connected ecosystem.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Hubtel Hosts Leaders of Dubai Chambers Ahead of New Horizon Investment Forum

May 15, 2026| 3-minute read

Hubtel Hosts Leaders of the UK Department for Business and Trade

April 10, 2026| 3-minute read

Cornell University Visits Hubtel To Understand Ghana’s Digital Economy

April 8, 2026| 3-minute read

Cornell University Visits Hubtel To Understand Ghana’s Digital Economy

Not every learning experience happens in a lecture hall. Sometimes, the most experiential education is a conversation with those doing the work and seeing for yourself.

For students from the Samuel Curtis Johnson Graduate School of Management at Cornell University, a visit to Hubtel offered precisely that kind of education: one that bridges the gap between the lecture halls and the field.

As part of a global experiential learning programme, the trip was designed to immerse students in the realities of innovation across emerging markets. What it delivered was something more valuable. It challenged the quiet assumption that digital economies evolve along predictable, universal lines.

In the classroom, digital ecosystems are often presented as structured systems governed by logic, scale, and rational adoption. On the ground, the reality proved more nuanced.

As discussions unfolded around Ghana’s fintech landscape, Augustine Adjei Gyawu, Head of Engineering, pointed to the pace at which digital payments have evolved, noting that “the ecosystem is not just growing, it’s constantly adjusting to how people choose to use it.”

In contrast to the structured models often presented in classrooms, Ghana’s fintech landscape revealed a more fluid dynamic. One defined by high volumes of low-value transactions, sensitivity to failed payments, and a constant negotiation between convenience and trust.

“You can build a technically sound product,” Patrick Asare Frimpong, Head of Product Management in Product & User Care, noted, “but if it doesn’t align with how people actually transact, it won’t scale.” His point underscored a broader reality of how product decisions are not made in isolation but are shaped by everyday user behaviour.

READ ALSO: Hubtel Empowers Next Generation Through AI Education Partnership with Brainwave AfricaTech

Bill Inkoom, Head of Mobile App Engineering, extended the conversation to financial inclusion, pointing to the role of digital platforms in expanding access, while emphasizing that adoption ultimately depends on user confidence and lived experience.

The session evolved into a genuine exchange, with students drawing comparisons across markets and interrogating how different systems respond to similar challenges. It reinforced the need that environments like this cannot be fully understood through case studies alone. They have to be experienced.

For the visiting students, Hubtel was not simply a company to study, but a case for rethinking how digital economies are understood not as systems to be mapped neatly onto theory, but as environments that demand closer, more critical attention.

In that sense, the most important lesson was not about Ghana’s digital economy alone. It was about the limits of certainty, and the value of seeing for oneself.

Warning: Constant COLOR_SCHEME_BLUE already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 3

Warning: Constant COLOR_SCHEME_RED already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 4

Warning: Constant COLOR_SCHEME_LIGHT already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 5

Warning: Constant FACEBOOK_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 8

Warning: Constant LINKEDIN_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 9

Warning: Constant TWITTER_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 10

Warning: Constant WHATSAPP_SHARE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 11

Warning: Constant CUSTOM_ADS_CONTENT_WRAPPER already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 14

Warning: Constant IMAGE_WRAPPER_CLASSES already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 15

Warning: Constant APPLE_APP_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 18

Warning: Constant GOOGLE_PLAY_STORE_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 19

Warning: Constant HUAWEI_APP_GALLERY_URL already defined in /var/www/html/bloghubtel/wp-content/themes/bloghubtel/template-parts/content-mobile-app-banner.php on line 20

Related

Hubtel Hosts Leaders of Dubai Chambers Ahead of New Horizon Investment Forum

May 15, 2026| 3-minute read

Hubtel Hosts Leaders of the UK Department for Business and Trade

April 10, 2026| 3-minute read

Hubtel Joins MTN to Combat Fraud Via Fintech Partner Exchange

April 9, 2026| 5-minute read